Three background questions

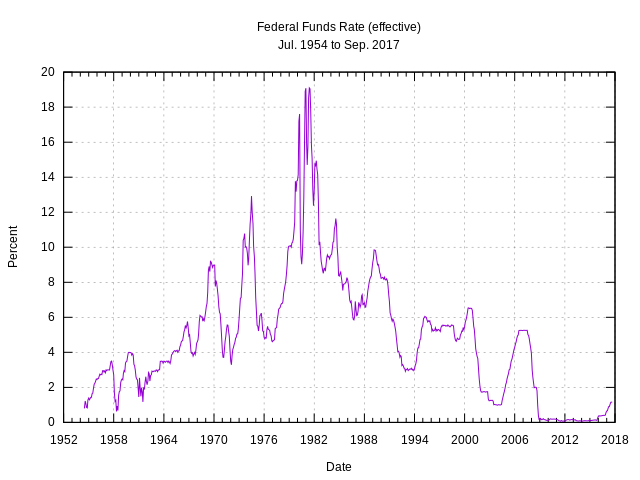

So, what is the Federal Funds Rate?

The interest rate at which a depository institution lends funds maintained at the Federal Reserve to another depository institution overnight. The federal funds rate is generally only applicable to the most creditworthy institutions when they borrow and lend overnight funds to each other. The federal funds rate is one of the most influential interest rates in the U.S. economy, since it affects monetary and financial conditions, which in turn have a bearing on key aspects of the broad economy including employment, growth and inflation. The Federal Open Market Committee (FOMC), which is the Federal Reserve’s primary monetary policymaking body, telegraphs its desired target for the federal funds rate through open market operations. Also known as the “fed funds rate".

While we are at it, what is the Federal Reserve?

The central bank of the United States. The Fed, as it is commonly called, regulates the U.S. monetary and financial system. The Federal Reserve System is composed of a central governmental agency in Washington, D.C. (the Board of Governors) and twelve regional Federal Reserve Banks in major cities throughout the United States.

So what does the Federal Reserve Do?

Current functions of the Federal Reserve System include:

- To address the problem of banking panics

- To serve as the central bank for the United States

- To strike a balance between private interests of banks and the centralized responsibility of government

- To supervise and regulate banking institutions

- To protect the credit rights of consumers

- To manage the nation's money supply through monetary policy to achieve the sometimes-conflicting goals of

- - maximum employment

- - stable prices, including prevention of either inflation or deflation

- - moderate long-term interest rates

- To maintain the stability of the financial system and contain systemic risk in financial markets

- To provide financial services to depository institutions, the U.S. government, and foreign official institutions, including playing a major role in operating the nation's payments system

- To facilitate the exchange of payments among regions

- To respond to local liquidity needs

- To strengthen U.S. standing in the world economy